Have you ever stopped to think about your personal financial standing, the true sum of what you own versus what you owe? It is, you know, a pretty big question that many people ask themselves, especially when they start looking at their money more closely. This idea, often called your net worth, gives you a simple, clear snapshot of your financial health at any given moment. It is more than just how much cash is in your wallet or what your bank accounts show; it includes so much more, giving you, in a way, a full picture of your financial situation.

Figuring out this number can feel like a big task, but it is actually quite straightforward once you break it down. Think of it as putting together a puzzle, where each piece represents something you have or something you need to pay back. When you add up everything you own and then subtract everything you owe, what you are left with is that single, very important figure. It is, basically, a personal balance sheet, helping you see where you stand and perhaps even where you are headed financially, which is pretty useful, if you ask me.

Knowing this figure is not just for big businesses or those with lots of money; it is something that everyone can benefit from understanding. It helps you make smart choices about spending, saving, and even your future plans. It is, after all, your own financial story, told in numbers, and it can be a really helpful tool for anyone looking to gain some control over their money matters, so it is definitely worth a look.

Table of Contents

- What Exactly Is Net Worth?

- Counting Up Your Stuff - The Assets of Net Worth

- What Do You Owe? The Liabilities in Your Net Worth

- Why Bother With Your Net Worth?

- How Do You Track Your Net Worth?

- Can Your Net Worth Data Ever Get Tricky?

- How Can You Improve Your Net Worth?

- A Summary of Your Net Worth Journey

What Exactly Is Net Worth?

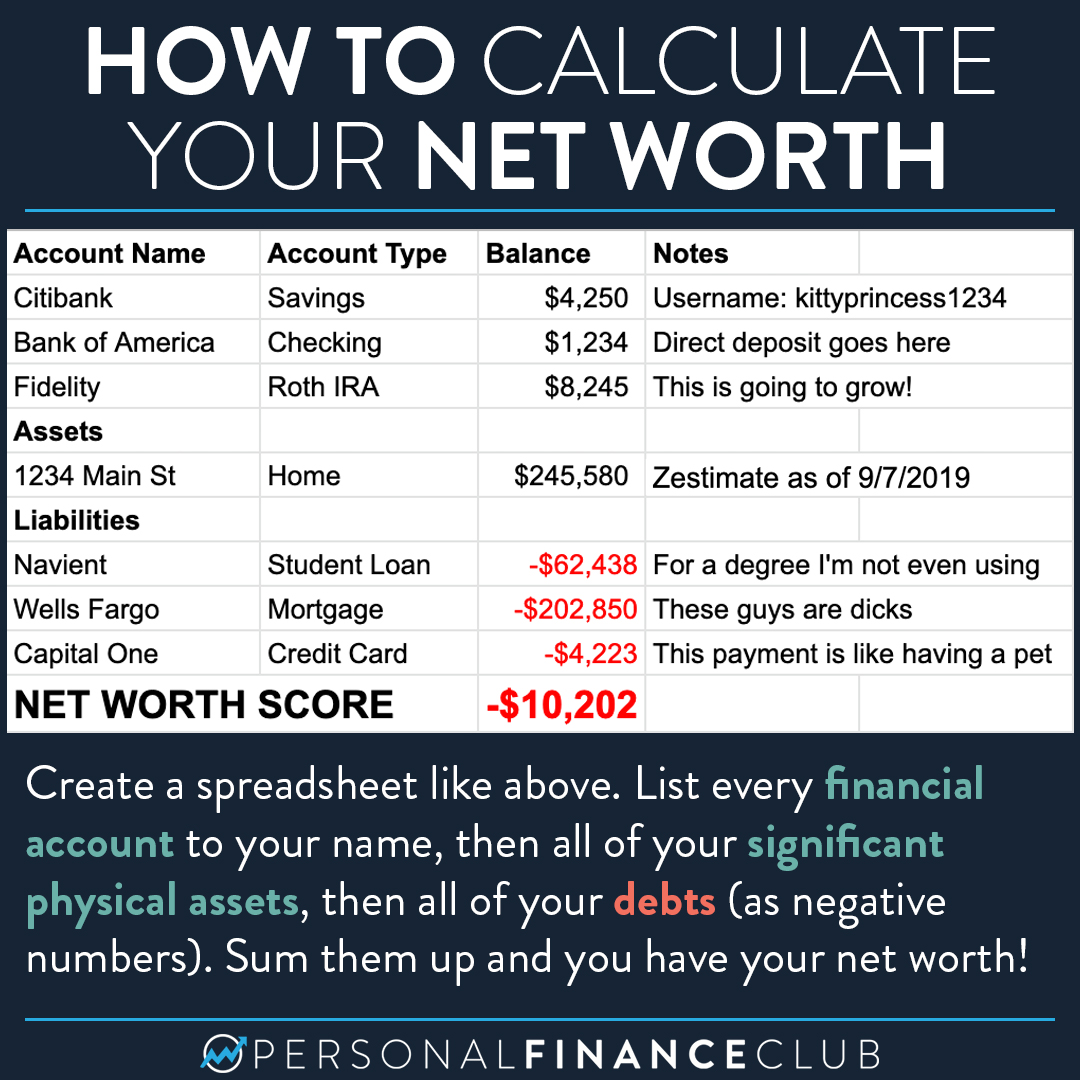

So, what are we talking about when we say "net worth"? It is, simply put, the difference between what you have and what you owe. Imagine you are doing a quick check-up on your money. You add up all the good things, like money in your bank accounts, things you own that have value, and any investments you might have. Then, you take away all the things that you still need to pay back, like money borrowed for a house or a car, or any credit card balances. The number you get after doing that is your personal net worth. It is a straightforward calculation, really, and it gives you a very clear picture of your financial standing at that moment in time. This figure can be positive, meaning you have more than you owe, or it could be negative, meaning your debts are currently bigger than your possessions, which is something many people experience at different points in their lives, too.

- January 25 2025 Planets Align Spiritual Meaning

- Images Drew Barrymore

- Net Worth Cher

- Who Was Howard Wife

- Special Needs Diapers

Counting Up Your Stuff - The Assets of Net Worth

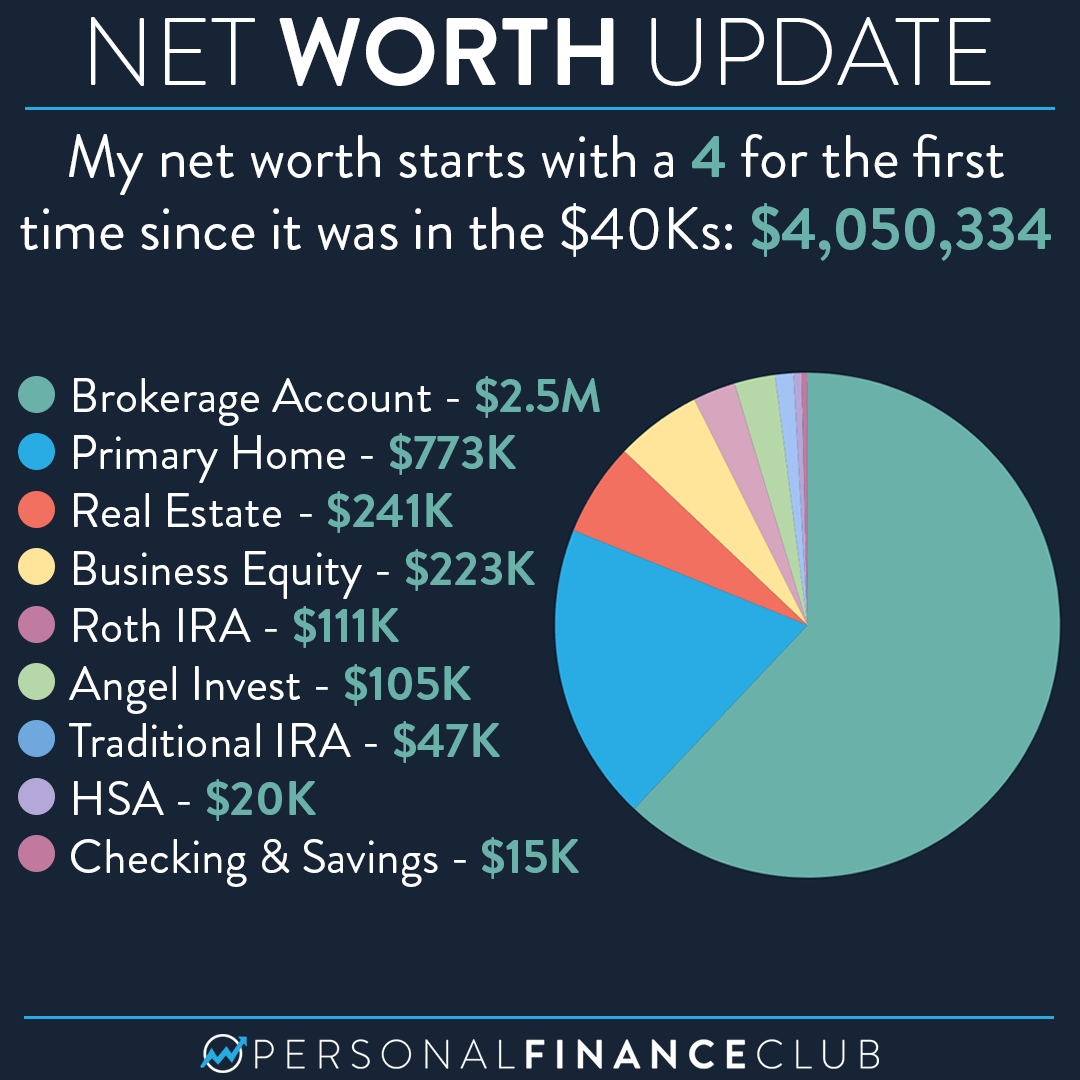

When we talk about what you "have," we are referring to your assets. These are all the things you own that hold some sort of value. For many people, this includes the cash sitting in basic checking and savings accounts. But, you know, it goes beyond just that. For instance, many people would also want to make sure they include the value of any real estate holdings in their net worth calculations. If you own a house, a piece of land, or maybe even a vacation spot, that property has a market value, and that value contributes significantly to your assets. You would, as a matter of fact, typically put this kind of property into your accounts ledger as an asset, like a record of something valuable you possess.

Beyond bank balances and property, there are other items that add to your net worth. This might include the money you have put into investments, like stocks, bonds, or retirement funds. These accounts, over time, can grow quite a bit, making them a very important part of your overall financial picture. Then there are things like vehicles you own outright, or perhaps valuable collections, or even certain personal items that could be sold for a good amount of money. Each of these items, in its own way, adds to the total sum of what you own, painting a fuller picture of your financial possessions, which is quite interesting to see when it all adds up.

What Do You Owe? The Liabilities in Your Net Worth

Now, let us talk about the other side of the coin: what you owe. These are your liabilities, the debts that you need to pay back. For most people, this includes things like a mortgage on their home, which is often the biggest debt someone carries. Then there are car loans, student loans, and any personal loans you might have taken out. Credit card balances are also a common liability, especially if you carry a balance month to month. Basically, any money that you have borrowed and still need to return counts as a liability, which is pretty clear, I think.

It is important to list all these debts, big and small, when you are figuring out your net worth. Sometimes people might forget about smaller debts, or maybe they just do not think about them as much as the bigger ones, but every bit counts. Even things like medical bills that have not been paid yet, or money you owe to a friend or family member, can be part of your liabilities. When you add up all these amounts, you get your total liabilities. This number is then taken away from your total assets to give you that final net worth figure. It is, in a way, like taking stock of everything that needs to be settled before you can truly see what you have left, so it is a crucial step.

Why Bother With Your Net Worth?

You might be thinking, "Why should I even care about this number?" Well, knowing your net worth is actually quite helpful for a few reasons. For one, it gives you a really clear sense of where you are financially right now. It is like a report card for your money habits. If your net worth is growing, it suggests you are doing a good job saving, paying down debt, or making smart money choices. If it is staying the same or going down, it might be a sign to look at your spending or earning habits. It is, basically, a very personal financial check-up, you know?

Also, tracking your net worth over time can be incredibly motivating. When you see that number slowly climbing, it can really encourage you to keep going with your financial goals. It is proof that your efforts are paying off. It can also help you make big decisions, like whether you can afford a new house or if it is a good time to change jobs. It is a tool for planning, really, helping you see the bigger picture beyond just your monthly income and expenses. It is, in some respects, your financial compass, guiding you.

How Do You Track Your Net Worth?

So, how does one actually go about putting this all together? There are a few ways, from simple to more involved. Many people start with a spreadsheet. You can list all your assets in one column and all your liabilities in another. For example, if you enter income from work, and then select the checking account as the place where you deposited it, you would want the corresponding account in the spreadsheet to show that increase. This kind of manual entry can be quite detailed, and it lets you see every single item. It is, you know, a very hands-on approach.

Some folks use financial apps or software that can connect to their bank accounts and automatically pull in information. This can save a lot of time, though you still need to make sure everything is categorized correctly. Sometimes, when you are adding details to a spreadsheet, the file might not respond, or you might find the file hidden but cannot open it because you cannot verify the file is okay. These little glitches can be frustrating, but they highlight the need for good data management, making sure your records are accurate and accessible. It is, basically, about finding a system that works for you and that you can keep up with regularly, perhaps once a month or every few months, which is pretty manageable.

Can Your Net Worth Data Ever Get Tricky?

Sometimes, keeping track of your net worth can run into a few bumps, you know, like when technology decides to be less than helpful. For instance, I remember someone trying to create a .pst file from an email address and then trying to put it into a new account, only to get the same message over and over again. Or, another time, trash folders only containing the last seven days of deleted items, while all the other folders held their data. These little hiccups, while often related to specific software or email issues, point to a larger truth about financial data: it needs to be accurate and complete to give you a true picture of your net worth. It is, basically, a reminder that the tools we use to manage our information can sometimes have their own quirks.

It is also worth noting that sometimes, even with the best intentions, things do not quite line up. For what it is worth, sometimes suggested solutions from support teams do not address specific problems, which can be a bit of a headache when you are trying to get your financial records in order. It is like when someone is not sure whether any attempts to fix something were successful. This means you might need to reach out for more help or try different approaches to make sure your financial information is truly reflecting your situation. It is, essentially, about being persistent and making sure your data is as clean and verifiable as possible, because a small error in one place can, in some respects, throw off your whole net worth calculation.

How Can You Improve Your Net Worth?

Once you know your net worth, you might wonder how to make that number grow. It is, in a way, pretty simple: you either increase your assets or decrease your liabilities. On the asset side, this means saving more money, investing wisely, and perhaps even looking for ways to earn more. Putting money aside regularly, even small amounts, can really add up over time. When you invest, your money has the chance to grow even more, which is a great way to build up your assets. It is, basically, about making your money work for you, which is pretty cool.

On the liability side, it is about paying down your debts. Focusing on paying off high-interest debts first, like credit card balances, can save you a lot of money in the long run. Every time you pay down a loan or a credit card, you are directly increasing your net worth because you are reducing what you owe. It is, in some respects, like giving yourself a raise, because that money is no longer going towards interest payments. This two-pronged approach – growing what you have and shrinking what you owe – is the most straightforward way to see your net worth climb. It takes time and patience, but it is definitely achievable, and quite rewarding, too.

A Summary of Your Net Worth Journey

To put it all together, your net worth is a very personal and useful financial measure. It is a simple calculation of everything you own, like your bank accounts, real estate, and investments, minus everything you owe, such as loans and credit card balances. This single number offers a clear picture of your financial standing at any moment. Tracking it regularly, perhaps with a spreadsheet or a financial tool, helps you understand your money habits and make informed decisions about your future. Even if you run into little technical snags with your data, the effort to keep your financial records accurate is, basically, very much worth it. By focusing on increasing your assets and reducing your liabilities, you can actively work towards improving your financial health over time, which is a pretty empowering thing to do.

- Chapel From Return To Amish

- Hamilton Current Cast Broadway

- Restaurants With Birthday Rewards

- Who Was Howard Wife

- Nephew Day